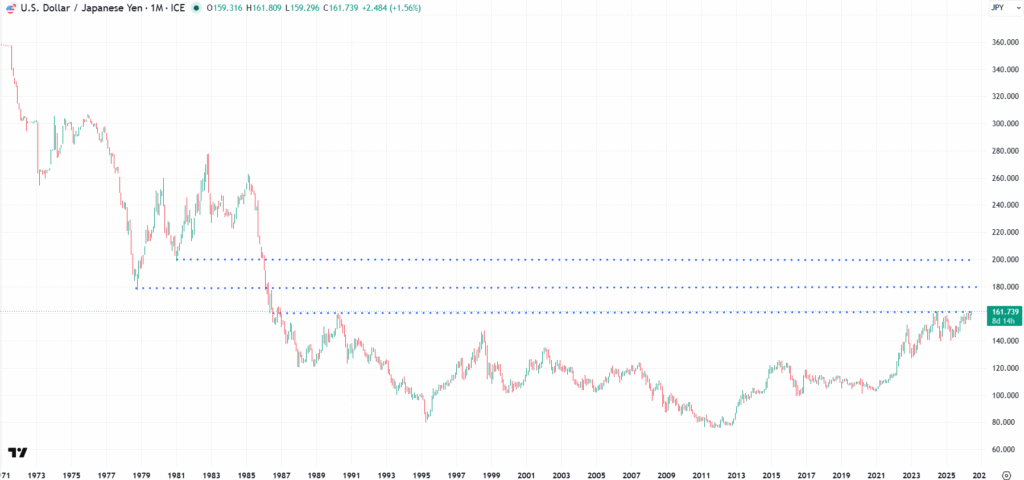

While everyone’s attention is polarized by anything involving the peace negotiations between Iran and the US, negotiations that, to be fair, have been more like a “these are my requests, take it or leave it” from Iran and “Ok ok, we take it” from the US, the JPY has been slowly but inexorably continuing to depreciate, with USDJPY trading at 161.55 as I write. This despite the Japanese government intervening twice on Monday during US trading hours as soon as the FX rate broke 161.90 after an emergency call to coordinate with the US Treasury (“Japan finance minister held emergency call with Bessent as yen nears 40-year low“).

If you ignore the fact that the JPY is trading at its weakest level of the past 40 years, and that the Bank of Japan just hiked rates to 1% (the highest since 1995), then everything is fine. If instead you consider that over $2 trillion equivalent of leverage in the global markets comes from the JPY carry trade, that the BOJ is moving like a snail to hike rates, and that Japan imports 100% of its crude oil, then you get goosebumps.

Everyone thinks that, if any fireworks are lit up, it will be in the Middle East. But what if the fireworks show starts in the complete opposite direction, taking everyone by surprise?

For years, I have been repeating that Japan is trapped in a monetary “doom loop,” and I even wrote a couple of articles on the matter, explaining it extensively, if you have time to check them out:

- THE JPY (COUNTERINTUITIVE) DOOM LOOP – THE MORE JPY LOSES VALUE, THE MORE LEVERAGE IS FORCED TO COME OFFLINE, THE MORE THE JPY LOSES VALUE

- EXPLAINING AND SIMPLIFYING THE JPY (COUNTERINTUITIVE) “DOOM LOOP”

In a nutshell, while the Bank of Japan continues to print money (fyi they never stopped QE; they just slowed it down a tad) to manage Japan’s massive debt, rising rates actually devalue the JPY because more money printing is required to cover the higher interest repayments. That devaluation forces investors in the massive JPY carry trade to post more collateral on their JPY FX swaps, which in turn forces them to borrow even more JPY to acquire collateral to cover losses. Once this self-reinforcing cycle maxes out, Japan will be flooded with liquidity coming back home, while foreign assets will be dumped, or fire-sold in case of stress, to repay the debts.

Another important factor I keep stressing is that, while people think Japan can sit comfortably on its pile of US Treasuries and foreign reserves (still the largest in the world), in reality it’s thanks to those reserves that the JPY still has some value for international investors.

Here the math is simple: if the BOJ continues to print JPY and Japan’s foreign reserves don’t increase, the ratio between them is going to rise, translating into more devaluing pressure on the currency.

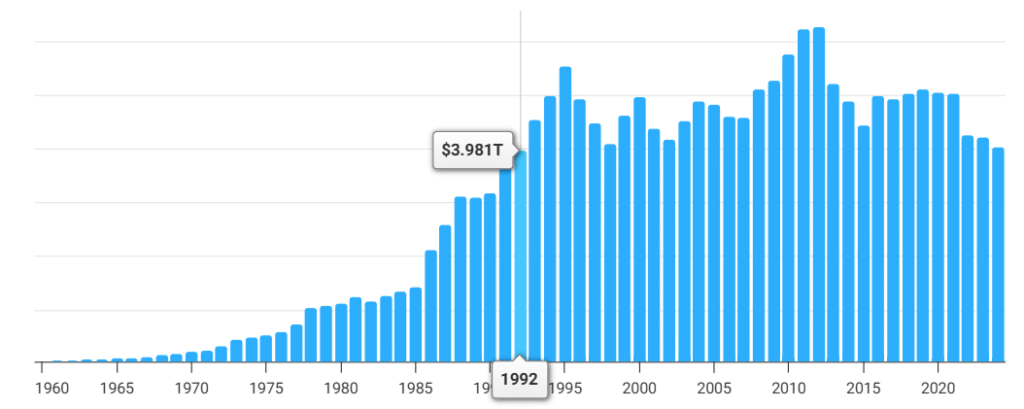

Some people tried to argue that the Japanese economy, after decades of stagnation, is growing again thanks to years of Abenomics and the series of stimulative policies that followed. Here is the mistake: confusing nominal growth in JPY with growth against the international yardstick, the USD.

As you can see in the chart below, in USD terms, Japanese GDP measured in USD is currently roughly the same as in 1992, or 34 years ago. Does it still sound surprising that the JPY is currently trading at its weakest value compared to the USD over the past 40 years?

Furthermore, the Japanese economy has been growing nominally in JPY. However, if you calculate the real level of inflation in the economy, rather than using the officially ridiculous one published by the government, Japan has been in recession since 2020.

Now, what happens if Japan sells its foreign reserves to strengthen the JPY? As I have been saying for years, and proven right every single time, any Japanese FX intervention is completely futile at sustainably strengthening the currency.

Why? Because the government is effectively selling the very same assets that are serving as “collateral” for the value of the JPY, a currency that continues to increase in supply because of the BOJ “QE infinity” and ballooning government debt that is currently at 236% of its GDP, a figure even greater than that of already broken countries like Venezuela.

Consequently, any JPY FX intervention is “exit liquidity” for all those investors looking to de-risk from the JPY, which is why it never took too long before the currency weakened back to the level it was trading at right before the government intervention.

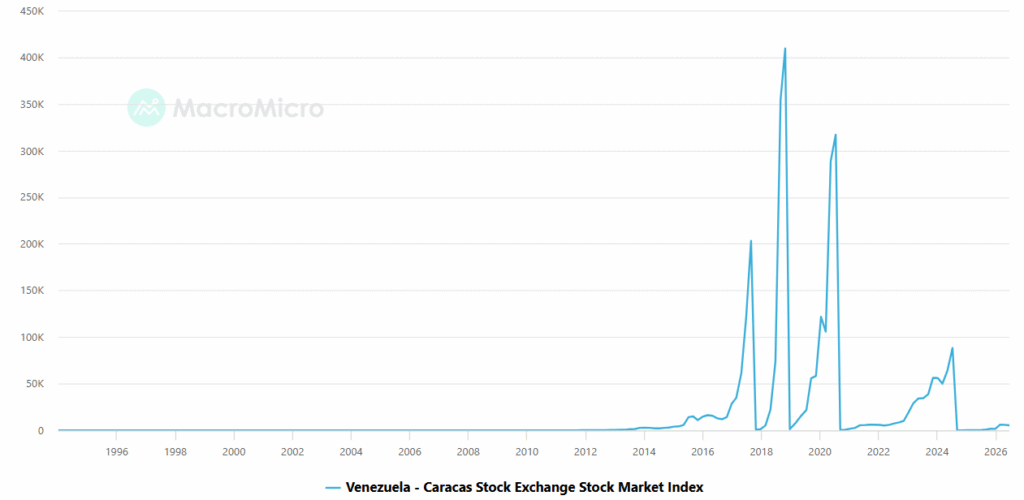

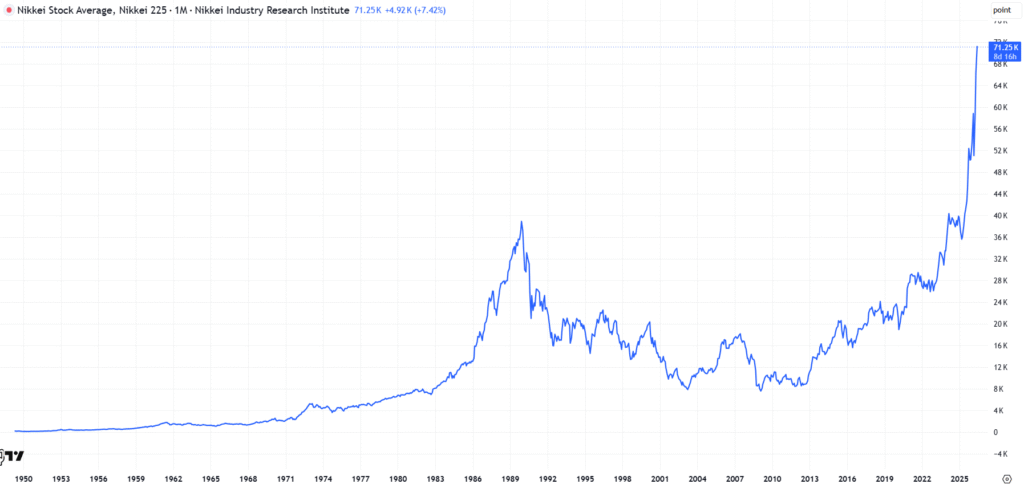

If you think the Nikkei breaking all-time highs day after day compensates for all this economic nightmare Japan is falling into, let me share with you the index of the Venezuelan Caracas stock exchange. Shocking, isn’t it?

Of course, the Venezuelan market is a far cry from the Japanese one; nevertheless, do you see any similarity with the Nikkei by any chance?

Two years ago I warned how, in the long term, it was inevitable for the JPY to weaken past 300 compared to the USD (”A PEEK INTO THE FUTURE: USD/JPY ROAD TO 300”), and we are now getting very close to the next stage of sharp devaluation that can potentially weaken the JPY past 175, especially if I am right and the upcoming oil price shock is going to throw gasoline on this fire. The next stop after that? 200.

The market loves to stare at the obvious fires because they make for great headlines. But the slow, structural accidents are the ones that wipe out portfolios, not because they are more dramatic, but because they are easier to ignore until it’s too late.

Japan is still stuck in the same loop: a debt load that cannot tolerate materially higher rates, a central bank that must keep manufacturing liquidity to keep the system upright, and a currency that pays the price for that choice. The weaker the JPY gets, the more inflation Japan imports through energy and commodities. The more inflation it imports, the more pressure there is to normalize policy. Yet the more it tries to normalize, the more the debt math deteriorates, and the more the market starts anticipating the next wave of printing.

At the same time, the carry trade is not some niche strategy. It is a pillar of global leverage and risk appetite. As long as the JPY is a cheap funding currency, investors will keep using it to buy everything else. But once the move becomes disorderly, the direction of capital flows reverses. Collateral calls do not care about narratives. They trigger forced deleveraging, and forced deleveraging does not stop at the border of Japan. It spills into everything from equities to credit to government bonds, and anything that was purchased with borrowed stability.

The popular assumption is that Japan can always defend the currency with reserves. The uncomfortable reality is that using reserves is like selling the last fire extinguisher to buy a few more minutes of oxygen.

So the question is not whether USDJPY can print 175 or 200. The question is what breaks first: the market’s willingness to fund the trade, the credibility of the policy framework, or the assumption that the next shock must come from the Middle East because that is where everyone is looking.

The most dangerous risks are the ones that feel boring, until suddenly they are not. If the next volatility event is driven by Japan, it will not arrive with a warning siren. It will arrive as a gap, a scramble for collateral, and a global selloff that looks irrational only to those who forgot where the leverage was funded. That is why this matters. Not because Japan is about to explode tomorrow, but because the fuse is already burning, and most people are watching a different fireworks show.