While I was waiting for Oracle numbers, a very interesting headline came out: “China plans $295bn state-directed AI buildout as Beijing moves to lock out Nvidia and AMD”.

This is what I wrote about 8 months ago in “THE DATA CENTERS FRENZY WILL BE REMEMBERED AS THE LARGEST WASTE OF CAPITAL IN HISTORY”:

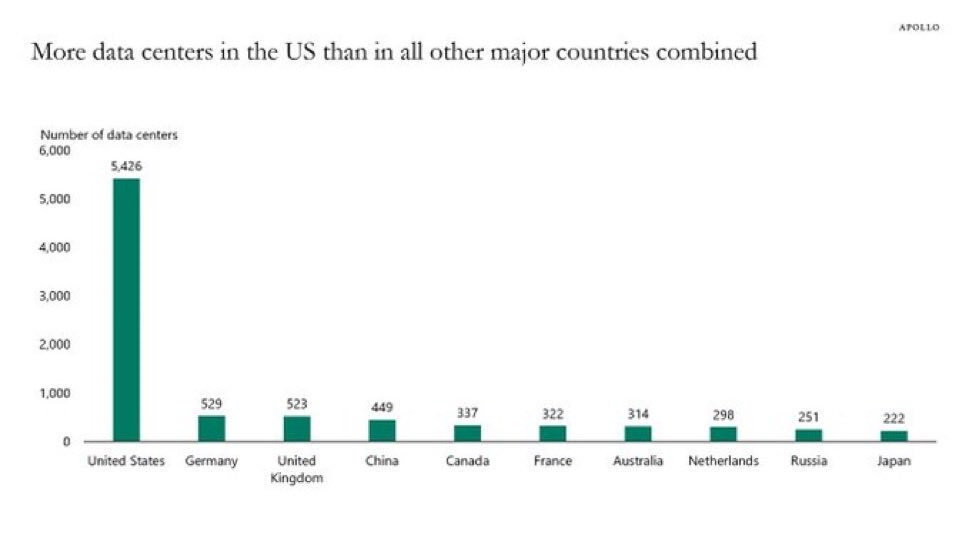

“As you can see in this chart, the number of data centers operational in the US right now is greater than all other countries combined and ten times higher than Germany, the second country by number of data centers.”

“Yet, nobody sees anything wrong with this. Let me ask a question: if there is a global AI arms race ongoing, then why aren’t all other countries participating?”

China, a country of 1.4 billion people and the second largest economy in the world, just committed to spending on building data centers over the next 5 years, roughly the same amount Google alone is expected to spend in one year. Furthermore, the strict condition to build data centers will be using 80% or more of domestically produced semiconductors. Is China doing this to protect Huawei and its other domestic companies, or is there something very wrong with how the whole AI data center buildout in the US around Nvidia, AMD GPUs at first, and now other alternatives like Google TPUs is developing? Of course, there is something very wrong with what has been happening in the US for many years now, and it never took a genius to figure that out; all that was needed was paying attention because the numbers never made any freaking sense.

Now that investors are starting to ask one simple question, “Why are you still not making much money after we gave you hundreds of billions of capital?”, you can notice all they can answer is “Trust me, bro.” This behavior is, unfortunately, not what lenders like to hear. Not surprisingly, you can observe how more and more companies are being refused new requests to borrow money and are instead forced to raise cash by issuing equity. Those that will still be able to entice lenders and not dilute their capital will only be companies with a sustainable business that can sustain an increasing debt burden.

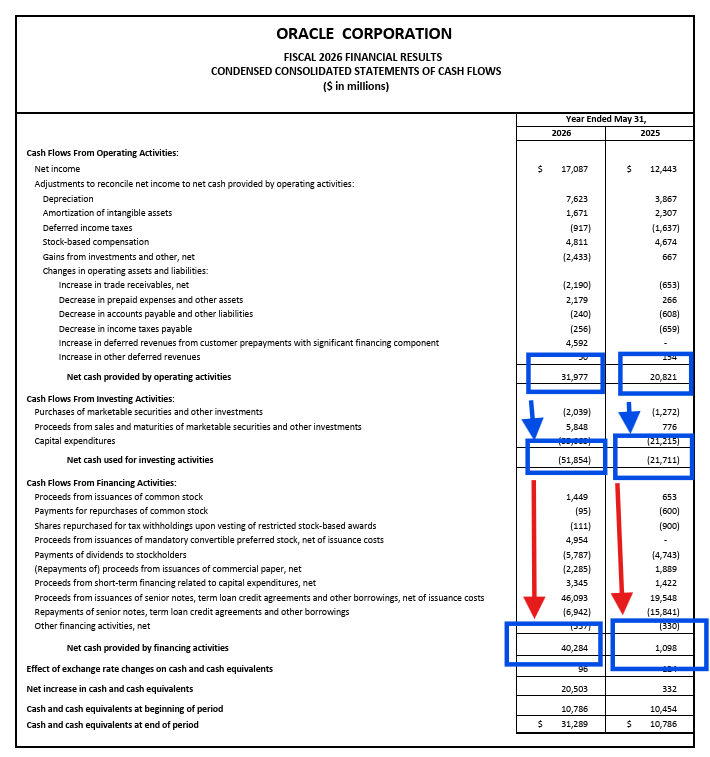

This is what the broader public is still not understanding: all these hyperscalers are not only throwing a biblical amount of cash into an incinerator, racing against each other in a “winner takes it all” competition rather than cooperating to share the infrastructure build-up (the Chinese approach), multiplying costs many times over, but they are also endangering their established and profitable businesses. Oracle is the most glaring example among all; just compare the cash flow numbers between FY 2025 and the FY 2026 just reported

In one column, you can see a software company venturing carefully into a new business. In the other column, you can see an infrastructure company with a software business attached to it. With the exception of Apple, you can observe the exact same trend among all the major tech mega-cap companies.

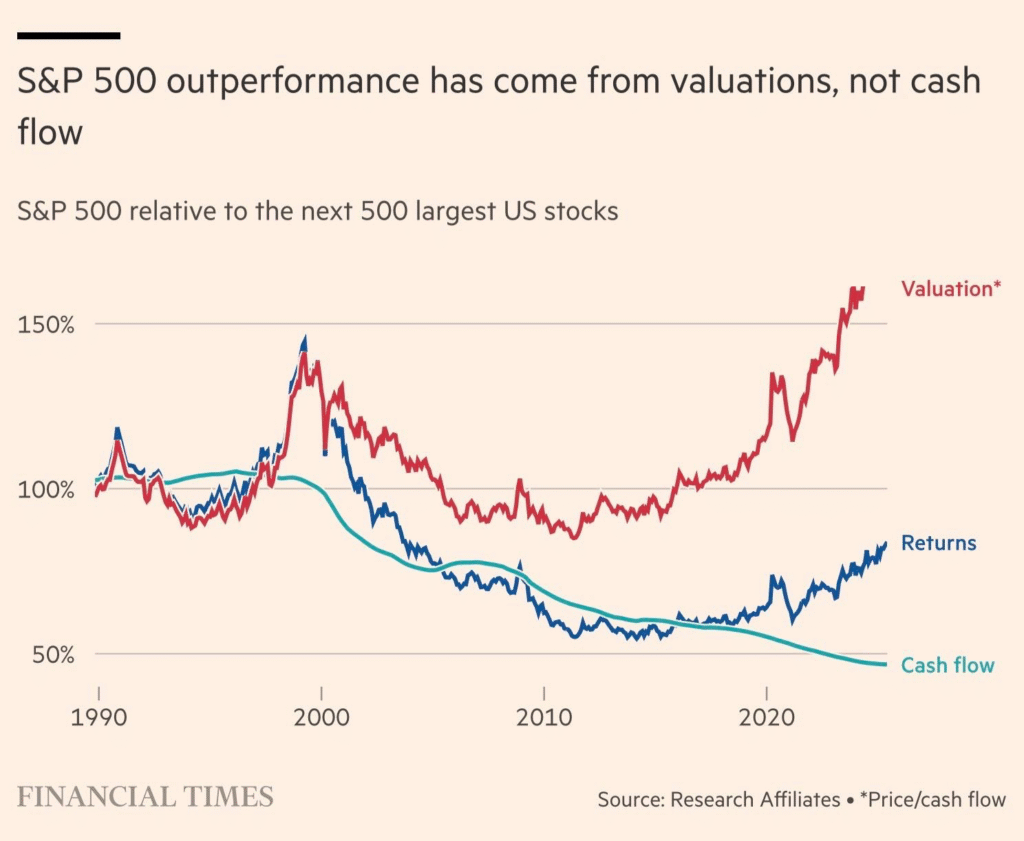

When you spent years convincing investors that you would have remained an “asset-light” cash cow business that would have granted them stable and long-term returns via dividends and buybacks because little of the cash you were generating needed to be reinvested to support your growth and market share, then it was somewhat fair to be valued at higher valuation multiples. However, if you pivot from “asset-light” to “asset-heavy,” you completely shatter your whole image in the eyes of investors, and when returns do not show up, people grow nervous and start punishing you in the market. This great chart from the FT perfectly summarizes what I just described:

There is another huge problem in what’s happening. Different from the Dot Com bubble times, when the infrastructure to connect the world to the internet would have remained useful for decades with little maintenance and replacements, the current build-up is in fast-depreciating, highly tailored infrastructure that requires huge maintenance and an impossible amount of resources, especially electricity, to operate. Costs that continue to rise, not even decreasing after many years, are a sign that its economics are going in the wrong direction with regard to what is required for the business of the whole industry to remain sustainable.

The last huge problem is that no companies that jumped onto this crazy bandwagon can afford to throw in the towel and give up. The crash in the stock price will be epic if that happens, to say the least, similar to what happened after META wasted tens of billions chasing the Metaverse. Mark Zuckerberg was lucky that he didn’t raise debt and impair the strength of his company operations while chasing the Metaverse dream; however, what’s happening now across the board is the complete opposite. The end of the story is already written: investors are tapping out, lenders are tapping out, and there isn’t enough cash in the markets to support everyone anymore. Google, Amazon, Microsoft, and Meta will be able to raise a little more because there is still a buffer in their legacy operations, not their AI business- but they will hit the brick wall too eventually. This time, though, don’t expect their valuations to quickly recover in the next cycle of FED quantitative easing that will be required to bail out the whole financial system, blaming the oil crisis because all these companies will be burdened by so much debt, write-downs, and legacy costs that any cash flow will be diverted to service their debt and remain in business, not to reward investors this time.