On Monday, after US markets closed, Alphabet (the parent company of Google) issued a press release that took investors by surprise (to say the least): “Alphabet Announces Proposed $80 Billion Equity Capital Raise to Expand AI Infrastructure and Compute.”

On the surface, Alphabet claims that, despite sitting on almost $127 billion of cash, cash equivalents, and marketable securities, and being projected to have yearly free cash flow north of $70 billion for 2026 (in line with recent years of reporting), this additional cash raised via equity issuance is meant to expand its AI infrastructure and compute. However, the devil is always in the details that people often forget to read; in this case, within the “Use of Proceeds” part of the press release:

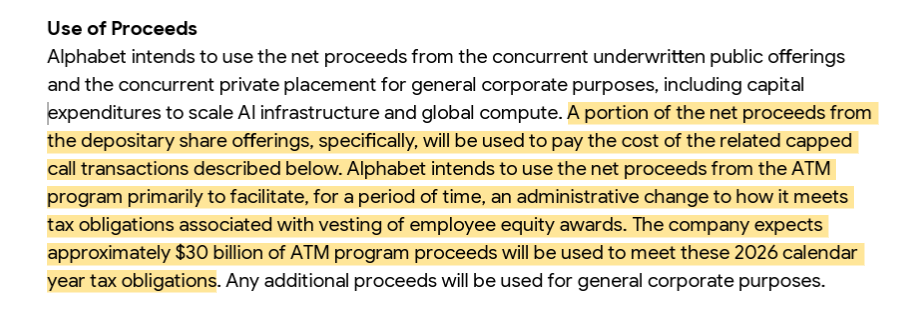

“Alphabet intends to use the net proceeds from the ATM program primarily to facilitate, for a period of time, an administrative change to how it meets tax obligations associated with vesting of employee equity awards. The company expects approximately $30 billion of ATM program proceeds will be used to meet these 2026 calendar year tax obligations.”

Let me explain what’s happening here. When Alphabet employees receive company stock as part of their pay, they must pay income taxes on those shares the moment they officially unlock. Usually, Alphabet covers this massive bill using cash from its own bank accounts, but for 2026, they’re trying a new administrative approach. They plan to raise up to $30 billion by gradually selling new stock directly onto the public market. Alphabet will then hand that cash directly to the government to pay off its employees’ tax bills, allowing the company to protect its own savings for other business needs. In a nutshell, Alphabet became a victim of its own success, or apparent success, that drove its market capitalization north of $4.5 trillion too quickly.

Because the stock price has climbed too quickly, the upcoming 2026 employee tax liability has ballooned to an estimated $30 billion. Usually, Alphabet would pay this bill quietly using cash from its own bank accounts. However, cutting a $30 billion check directly to tax authorities would heavily drain the company’s liquid reserves and undermine its CAPEX commitment plans, now at $180-190 billion for 2026 and expected to be even larger next year.

Allow me a fair question now: how many companies are currently in the same position as Alphabet? Apparently, Alphabet’s tax situation is unique, while the one for other major tech giants seems more manageable, according to my calculations based on current stock prices:

- Meta Platforms ($7.15B Tax Expense): Meta relies heavily on RSUs (Restricted Stock Units) to retain senior AI engineers. Because Meta’s stock has surged to around $610 per share, its annual equity pool is valued at over $20 billion. Unlike Alphabet, Meta covers this using its massive operational cash flows and actively neutralizes employee share dilution via its own aggressive stock buyback programs.

- Amazon ($6.81B Tax Expense): Amazon historically favors equity-heavy packages over high base salaries. With a $19.4 billion SBC (Stock-Based Compensation) footprint, it represents the second-largest tax liability on this list. Amazon handles this through standard net settlement, delivering the remaining 60-65% of unlocked shares to employees while paying the rest to the government out of cash reserves.

- Microsoft ($4.19B Tax Expense): Microsoft maintains a large employee base but structures compensation with a higher mix of baseline cash compared to pure-play social media or ad-tech firms. Its $11.97 billion stock expense translates into a highly manageable $4.2 billion tax bill, easily absorbed by Azure’s high-margin recurring cloud revenues.

- Nvidia ($2.24B Tax Expense): Despite trading at a massive $5.2 trillion market cap, Nvidia keeps its headcount relatively lean compared to software aggregators like Amazon. At $6.39 billion in annualized SBC, its tax withholding requirements can be easily scaled out of its hardware profit margins.

No need to worry too much then? Not so fast, my friend.

In the same press release, Alphabet claimed its enormous investments are required to “meet its unprecedented customer demand.” While a few months ago nobody would have dared argue against this statement, today the narrative strengthening in the mainstream media is quite the opposite, ultimately confirming the truth about AI demand I have been warning about for years: demand for AI was inflated by a widespread and sophisticated circular-financing and revenue round-tripping scheme among the biggest players in the industry:

- How Circular Financing Is Fueling the AI Boom

- AI’s Financial Circle Game

- Circular AI funding deals could pose ‘systemic’ risk, IMF warns

- Uber Caps Usage of AI Tools Like Claude Code to Cut Costs

- Microsoft reports are exposing AI’s real cost problem: Using the tech is more expensive than paying human employees

- Starbucks retires AI inventory program after just nine months

- What smart people are saying about rising AI costs

So far, since the beginning, it has been calculated that over $1.4 trillion has been spent on the AI buildup that, in three and a half years, barely generated $700 billion of revenues, of which the lion’s share, about $500 billion, flew into Nvidia’s coffers. Two weeks ago, I wrote “NVIDIA IS NOW VERY CLOSE TO HITTING THE CIRCULAR FINANCING BRICK WALL”, which is why I was not so surprised to read about Alphabet now tapping the equity market in an effort to keep the whole circular-financing scheme going. However, this move also signals something nobody is still publicly acknowledging: lenders’ capability to continue financing the AI buildup is near exhaustion.

Without lenders queuing to finance the purchase of data centers and GPUs, most of which are still sitting in warehouses rather than being operational as simple math dictates (data centers are being built at a slower and slower pace, with only a fraction of those due to be completed by 2027 even under construction), the $2 trillion of additional funding needed to bring the current AI setup to a scale where it becomes profitable and sustainable is likely nearing the end of what markets can provide.

Personally, I expect there will be more shots left, like Nvidia issuing debt to finance its customers’ AI buildup. Something so far avoided because its customers enjoyed ample access to capital markets, but lenders are growing skeptical now that returns are failing to show up, increasing concerns about whether all that debt granted so far can be repaid in full.

All I just described is unfolding at the same time the world is going through the biggest crude oil supply shock ever experienced in history. A shock so far successfully mitigated by the incredible amount of Strategic Petroleum Reserves and commercial inventory drawdowns ever. However, this cannot continue indefinitely. With energy prices set to rise sharply in the coming months, the impact on the whole AI sector that was already struggling to source cheap and abundant electricity even before the war in the Middle East started to power its energy-hungry data centers will surely be brutal. This is somehow a scenario nobody is pricing into the current market, but they will soon be forced to.

Alphabet’s $80B equity raise is less about “more AI” and more about managing a massive, near-term cash obligation tied to employee stock taxes, without draining reserves needed for capex. At the same time, it’s a warning sign that easy financing for the AI buildout is tightening just as energy costs are poised to rise. If lenders and customers pull back, the next phase of the AI cycle won’t be driven by hype or headlines, but by who can fund, power, and monetize compute at scale. A goal that so far does not seem realistically within the reach of even the largest hyperscalers.