It has been more than 2 weeks now since the war against Iran started, and so far, nothing has gone as planned. Literally nothing. Iran’s counteroffensive capabilities have been underestimated. Its willingness to cause severe damage to its enemies and allies economies was ignored. The overall impact on the global economy of a new, asymmetric type of warfare has been totally overlooked. Allow me to state some facts:

- The worst oil supply shock IN HISTORY is currently ongoing, with up to 15 million oil barrels of supply suddenly offline.

- Almost 20% of the total natural gas supply is now offline, and once the situation normalizes, it will take months for Qatar to restart its operations to full production capacity.

- 33% of the total supply of fertilizers is currently stuck in the Strait of Hormuz, with countries like China currently enforcing strict export controls on fertilizer exports.

- The damage to the entire oil supply chain around the Strait of Hormuz is not only still hard to quantify, but it is worsening every single day.

- Despite the IEA’s efforts to coordinate the quick release of 400 million barrels of oil from the SPR, of which the US will account for 172 million, technically, the flow of oil that can be released into the system to compensate for the missing supply from the Middle East is at best 5 million barrels a day.

The situation is objectively catastrophic for the world economy. Reserves of jet fuel are already running low in several countries, causing sharp spikes in prices. Prices of fertilizer have already jumped 35% in the past weeks. Production of other critical commodities like aluminum has already been disrupted as a consequence of some of the largest smelters in the world, based in the UAE, being shut down.

However, the nonstop message spread through social and mainstream media channels is “everything is fine,” “don’t worry, we’ve got it all under control,” “there is no need to panic.” Come on, let’s be serious. This is such an incredible mess, and the chances of a quick solution with normality being promptly reestablished are now objectively ZERO. Yet, financial markets are still cruising as if almost nothing happened. After a brief scare, stocks still remain near all-time highs. Oil, natural gas, and other commodity prices increased in the past two weeks, yes, but nowhere near the level where the bare laws of demand and supply equilibrium would dictate.

Isn’t what I just described already so eerily similar to the onset of the Covid crisis? Yes, but with one difference. The Covid crisis was an induced economic shutdown as a consequence of lockdowns, while this time around, the economy is facing a slowdown, if not a forced shutdown, in some of its most critical parts. The consequences of all I described aren’t yet visible to all those not living in the Middle East, especially with regard to oil, thanks to the release of SPRs and to the available amount of oil supply that was already sailing towards its destination after the Strait of Hormuz was effectively closed. That amount of oil stock is going to be used up in about a week, according to the most reliable estimates. Afterwards, there will be a shortage of 10 million barrels of oil a day that cannot be compensated for with any other quick measure.

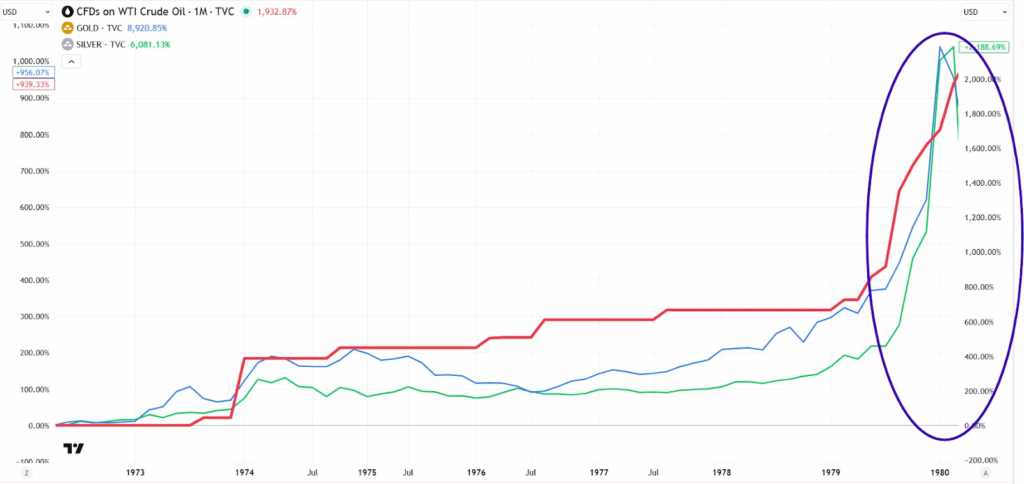

By the look of it, again similar to Covid, the market setup is bound to remain stable until the following OPEX since the economic shock triggered. The date this time is the 20th of March. Afterwards, we enter a very important week since the following one will be the end of the first quarter of the year, with a ton of window dressing at play. So far, investors have avoided shifting into a risk-off posture, paradoxically avoiding or even selling “safe haven” assets such as T-bills, cash, gold, or silver while relentlessly buying the dip in stocks, confident that, like last year and every time before, a quick solution for the benefit of preserving the biggest stock bubble in history could be found. What are the chances that the conflict with Iran ends by Friday? Virtually zero. As a consequence, it is logical to expect investors to start protecting their portfolios next week and prepare for the impact of a conflict, causing incredible damage to the global economy, to last longer than expected. Likely months, hopefully no longer than that, otherwise a repeat of the 1979 scenario with oil prices spiking 4 times in a few months, followed by a spike in gold, silver, and other commodity prices tied to strong inflation dynamics, becomes more and more probable.

Traders are betting central banks can hike rates and offset a huge flare-up in inflation, again similar to what happened in the 1970s. But guess what? While all I just described is happening, the $1.8 trillion private credit bubble is already imploding, and soon that credit crunch will cascade onto consumer credit, corporate loans, and likely high-yield bonds. There is no chance that central banks will have any room for maneuver to hike rates in such a situation.

The conclusion is inescapable: we are standing at the precipice of an economic catastrophe that could dwarf the COVID-19 shock in both scale and duration. The convergence of a historic energy crisis, collapsing credit markets, and geopolitical instability has created a perfect storm that no amount of central bank intervention or market optimism can wish away. The disconnect between financial markets and economic reality cannot persist much longer.

SYNNAX PROMO

Get exclusive intelligence on stocks you can’t find anywhere else – insights that could give you a serious edge. Claim your free Synnax trial month now:https://synnax.app/PROMO/JUSTDARIO