I don’t know whether, by the time I publish this article, anything I say will still be relevant given the current circumstances, but I hope most of the information will still be useful.

Let me start with gold and silver, whose long-term fundamentals are strengthening every day, but which, in the short term, won’t be able to escape market turbulence all that much. Why? Let me start by reminding you of what I warned about over a month ago in the podcast “GOLD AND SILVER ARE FACING THEIR WORST ENEMY: A LIQUIDITY CRISIS”: countries in the Middle East, especially the UAE, are going through a severe USD liquidity crisis, not only because their USD inflows have collapsed due to much lower amounts of crude oil being sold, but also because HNWI, foreign residents (90% of the population in Dubai), and foreign institutions are moving their assets and liquidity away from an area that will be considered a war zone for quite some time, ultimately resulting in big USD liquidity outflows, especially when all the currencies in the area are strictly pegged to the USD.

Not surprisingly, one month later the UAE, which, let’s not forget, last year pledged to invest up to 1.4 trillion USD in the US economy (”UAE commits to $1.4 trillion investment framework in US”), is now asking for a currency swap line from the US itself, which in monetary terms is the equivalent of requesting a bailout (”U.A.E. Asks U.S. About a Wartime Financial Lifeline”). The situation is clearly worsening, and the longer the Strait of Hormuz remains practically shut, the worse the situation is going to be. Furthermore, with the ceasefire now hanging in the balance, the likelihood of a second, more intense round of military confrontation is increasing by the hour, despite President Trump unilaterally declaring an “indefinite ceasefire” until a peace agreement is reached (”Trump declares Iran ceasefire extension with peace talks in doubt”).

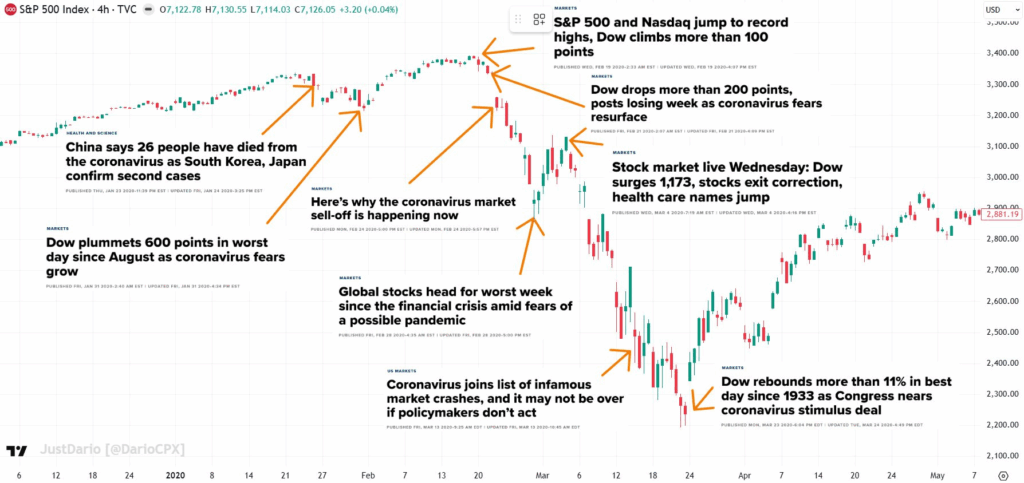

Here is where things start to bother me, truly, a lot. As reported by both the FT and Bloomberg, traders are now relying on Trump’s Truth Social posts almost exclusively to run their trading strategies, especially their trading algorithms. What’s wrong with this? When these posts have been proven not to carry fair and reliable information, but pure lies, people should have already learned to take anything coming from that direction with a grain of salt. However, this is not the case, and here we are with stocks back at all-time highs; sentiment indicators like the CNN Fear and Greed Index flashing “greed” again; oil prices that never came close to trading around the all-time high price reached last time back in 2008, despite the worst oil supply shock in history already having hit and even worsening (”This is the worst oil crisis in history”); and the whole financial system erupting with euphoria and FOMO like never before. Does what I’ve described ring a bell? For those who have a good memory, it should; for those who don’t, I made this chart to show what happened ahead of the 2020 market crash, pinning all the headlines steering market sentiment at that time.

Let me be clear once again: this is a market that cannot be shorted. Why? Because there is too much liquidity in the system, and rest assured that a lot more liquidity will be printed out of thin air to inflate economies and asset prices back up to compensate for the damage from the war in the Middle East. Shorting a market like this requires such a degree of timing precision that it’s easier to win the lottery; the risk/reward of such a trade is very poor. It is not a coincidence that Warren Buffett is currently sitting on almost $ 400 billion, waiting for the exact moment to buy assets cheaply when this ginormous bubble implodes. He is effectively demonstrating how sitting out with ample liquidity is the modern way to “short”.

Dear readers, we are in a regime where headlines and social-media narratives move markets faster than fundamentals, while the underlying system is becoming ever more dependent on fresh liquidity to paper over real economic damage. In this environment, gold and silver may continue to be buffeted by volatility and dollar-driven liquidity squeezes in the near term, but their long-term case strengthens as confidence in policy, data, and price discovery erodes. Government bonds, which, let’s not forget, are the equivalent of fiat money in the future, are surely one of the worst possible investments, especially when governments across the globe not only have little intention to rein in their deficit spending, especially the US, but are even actively capping yields while inflation in the real world rages.

This market can stay irrational and liquid longer than most traders can stay solvent. The prudent stance is to prioritize resilience: keep ample liquidity, avoid leverage, and build positions with a time horizon that can tolerate turbulence. When the cycle turns, as it eventually will, patience and capital preservation will matter far more than the ability to predict the next Trump’s post, the next headline, or the next spike.