HSBC Q1-25 financial earnings have just been released and despite a 25% earnings drop compared to the previous year, the market couldn’t resist rewarding the bank, sending its shares higher (~2% at the moment) for announcing its first interim dividend of 2025 and, most importantly, for increasing its share buyback commitment from $2bn to $3bn. Is anyone surprised? I believe not.

As I flagged in my last article on the lender (“WHAT HSBC ISN’T TELLING US: UNCOVERING THE RED FLAGS AND HIDDEN RISKS IN THEIR Q3 REPORT“), the bank continues to see an impact on its profitability in this current rates environment due to increased funding costs. However, once again, the bank had to work hard to hide the giant hole in its books to conceal the true extent of the difficulties it was going through. Unfortunately, this time the bank messed up with the numbers, as I am about to show you.

HSBC reported $876m as allowances for expected credit losses for Q1-25, down from $1.36bn in Q4-24. Besides this number continuing to be ridiculously low compared to the $1.9 trillion size of the bank’s balance sheet – and even more ridiculous if we add the off-balance sheet items that bring the total to $2.6 trillion – this trend in ECL is completely disconnected from the assumptions the bank itself uses to calculate its credit risk.

First of all, it’s worth noticing how, despite the deteriorating economic environment, HSBC increased the total size of its credit exposure (including off-balance sheet items) from $2.5 trillion in December 2024 to $2.6 trillion by the end of March 2025, while increasing the total allowance for ECL from $10.2bn to $10.6bn, equivalent to 0.40% of the total credit exposure in Q1-25. I apologize, but I am not even sure how to comment on this objectively meaningless figure.

Secondly, in an incredible display of inconsistency, while the bank increased its exposure to risk and decreased the allowance for ECL this quarter compared to the previous one, it justifies the move based on its own economic assumptions that showed worsening across major economies in terms of GDP in 2025 and inflation in the next 5 years, even though the bank improved their forecasts for economic drivers such as unemployment and house prices – with one exception: China. I know this is such a brain-twister, right? Let’s look at this in more detail.

- With regard to the UK, US, Hong Kong, France, and Mexico, the bank decreased its GDP forecasts from 1.2%, 2%, 1.7%, 0.9%, and 0.9% in Q4-24 to 1.1%, 1.8%, 1.5%, 0.7%, and 0.2% respectively in its “consensus-based scenario”. What about China’s GDP growth expectation in 2025? The bank increased its GDP expectation from 4% to 4.5%. However, despite these revisions, the bank played around with forecasts, keeping the average for the next 5 years unchanged and broadly bullish, ignoring the economic slowdown recorded already in the last months of 2024 and the incoming threat of tariffs by the US administration already manifested during Q1-25

- With regard to forecasts of unemployment and house prices, the bank broadly increased its 5-year average growth expectations for the current quarter, in complete contrast with all the economic data that kept coming in.

- Lastly, even though the bank broadly increased the 5-year average inflation across the board, it did not make changes to its prediction of central banks’ policy rates whatsoever.

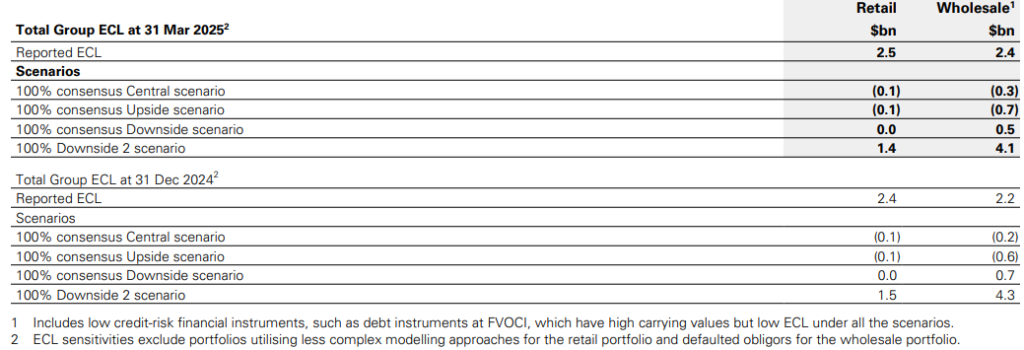

Similar adjustments have been made to its upside, downside 1, and downside 2 scenarios that, in the worst case, only predicts a brief economic contraction in the next 5 years across the board. HSBC predictions aren’t bullish, but super bullish – as a matter of fact, I believe we all agree with that. As you can see in the table below, the bank only expects an additional $5.5bn in ECL in the worst-case scenario, $300m lower than what it expected 3 months ago.

At this point, we can conclude without a shadow of a doubt that HSBC is playing heavily with its Mark To Market estimates to portray a much healthier state of its books than what they are in reality. What is the true extent of the losses then? As we discussed in “BANK OF AMERICA’S Q1-25 EARNINGS: MORE SMOKE AND MIRRORS TO HIDE ITS INSOLVENCY“, BAC holds $100bn of unrealized losses alone, mostly on MBS. HSBC doesn’t hold as many MBS as BAC but holds a similar exposure to Commercial Real Estate and Residential Real Estate in Hong Kong, Mainland China, and the UK, against which it has only put aside a negligible allowance for ECL so far (the bulk likely against Evergrande and Country Garden real estate developers). Overall, a rather conservative estimate puts HSBC’s unrealized losses between $50bn and $75bn already, a far cry from the $10.6bn allowance from ECL the bank put aside and far from the losses they expect if their worst-case scenario materializes. Clearly, the bank is lying through its teeth to give an impression that “everything is awesome” despite the poor shape of the bank that pushed its former CEO to abruptly resign in May last year. How long can this go on until reckoning with reality becomes inevitable? I will leave this question open to everyone’s consideration.

JustDario on X | JustDario on Instagram | JustDario on YouTube