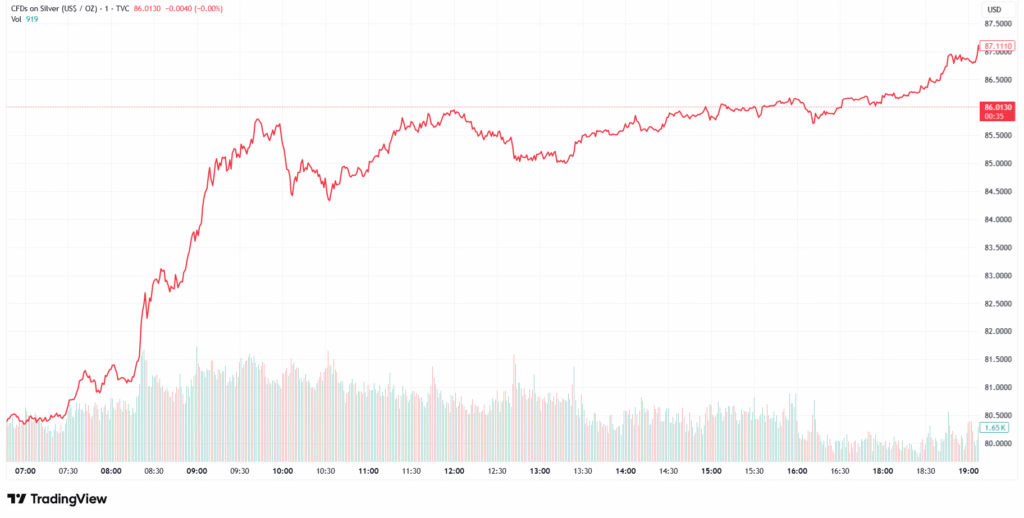

What a great day Monday was for Silver investors, with the metal trading as high as 87$, up more than 7% on the day, while the rest of the market, from gold, to bonds, to stocks, was broadly flat.

While I’m feeling pretty happy about the nominal gains in my portfolio, I’ll still be cautious for a little longer before resuming my stacking. Here are my reasons.

First of all, Silver is currently trading in contango, not in backwardation. This is a signal that, at this stage, unlike what we observed from October 2025 to March 2026, the market is not perceiving any scarcity of physical metal right now.

While the gap between supply and demand for silver persists, the reason the physical scarcity problem has been tamed is mostly thanks to the actions taken by the Shanghai Futures Exchange to protect Chinese industrial buyers:

- Zero Delivery Allocation for Non-Hedgers: Starting at the end of February 2026, the SHFE announced that participants without approved hedging quotas would receive zero delivery allocation on certain silver contracts.

- Targeting Near-Term Contracts: The restrictions specifically targeted near-term silver futures, requiring hedging positions in the delivery month and the month before to be approved, otherwise they were set to zero contracts.

- Focus on Industrial Users: The policy was designed to restrict physical silver access to genuine industrial hedgers, preventing speculators from taking physical delivery during a period of supply scarcity.

- Automatic Conversion of Positions: For all silver futures contracts, starting from the last trading day of February 2026, non-futures company members and overseas special non-broker participants without specialized approvals had their general-month hedging transaction limits for the near-delivery months automatically converted to 0 contracts.

These measures, combined with broader Chinese government export licensing requirements for silver starting January 1, 2026, fundamentally shifted the market, prioritizing local manufacturing needs (such as solar panels and electronics) over speculative physical demand.

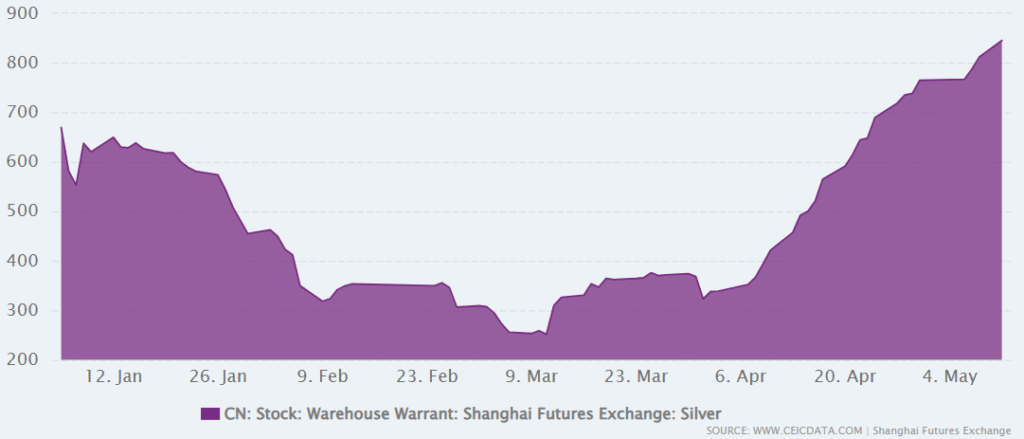

Not surprisingly, SHFE silver vaults started to record a steady increase in physical silver after almost being completely depleted in February.

Let me be clear: while this is “bad news” in the short term, the truth is that this move by China made the silver market stronger and more resilient in the long term, effectively creating a futures market that is more and more backed by real metal, and not by emptier and emptier promises like the Comex or the LBMA.

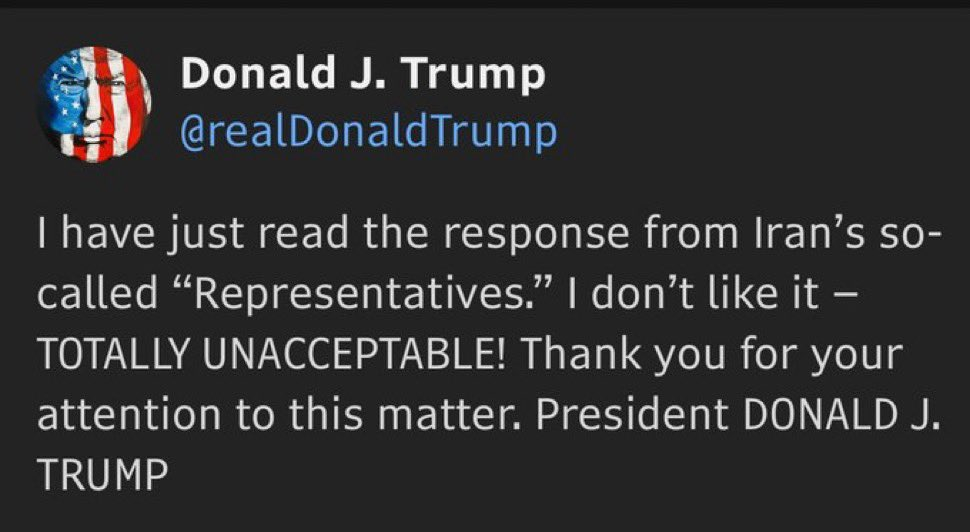

The second reason I prefer to remain cautious on silver for the time being is the Damocles Sword of the Strait of Hormuz still hanging above the head of all financial markets. On Sunday, Iran shared its answer to the US peace proposal and, not surprisingly, its demands were promptly rejected by President Trump.

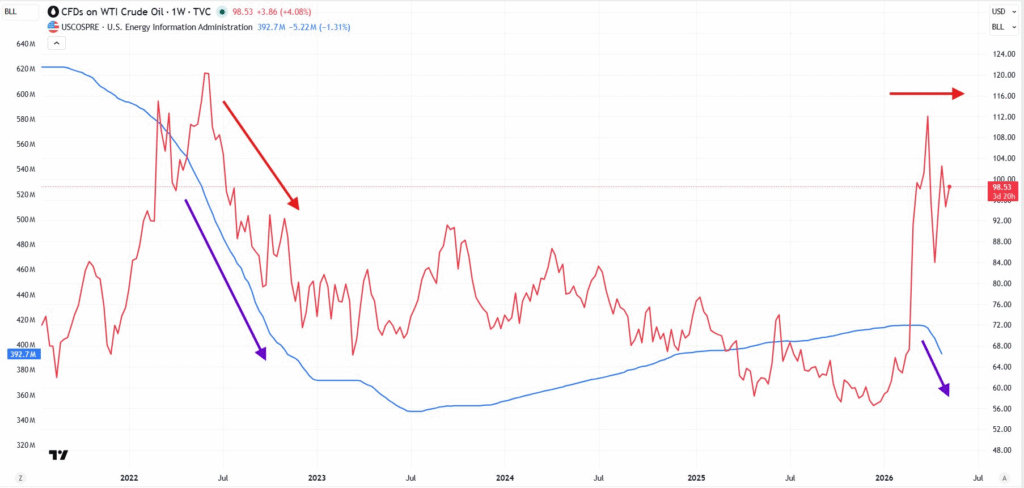

While this outcome was obvious to me from the beginning, and I never changed my mind about it, traders and investors moved on a while ago from factoring in any disruption risk to economies and markets resulting from the worsening mess in the Middle East. Surely, one thing that has been very effective so far in reassuring everyone is the successful oil price manipulation campaign implemented by the US government in coordination with its allies. Here is the problem, though. As you can see in this chart that compares the oil price with the trend of US SPR releases from 2022 till today, this price manipulation campaign is just “buying time.”

Why? If you step back and compare the playbook, the cynicism becomes even clearer. In 2022, Biden dumped the Strategic Petroleum Reserve into the market in the absence of a true supply shock, explicitly to push prices down and buy relief from an inflation crisis. In 2026, Trump is doing something far more desperate: leasing the SPR into the market even as the biggest oil supply shock in history begins to unfold, not to solve the problem, but to mask it for as long as possible.

As a matter of fact, the true oil supply shock hasn’t occurred yet. Considering that Trump is now only left with deciding between trying to keep the naval blockade on Iran in place, in the hope that it chokes its economy and pushes Iran to fold, and resume the military confrontation, forcing Iran to agree to the US peace deal requests forcefully (if successful), there is currently NO SCENARIO LEFT IN WHICH THE STRAIT OF HORMUZ SWIFTLY AND FULLY REOPENS FOR TRANSIT AS IT WAS THE CASE TILL THE 27TH OF FEBRUARY. Period. As a result, there will be another burst of volatility in financial markets sooner or later, either caused by the strain put on global oil reserves heading closer and closer to “tanks bottom” if global demand does not adjust accordingly by then, or by a resumption of the military conflict where the US is not assured to be the certain winner at all.

Such a spike in volatility, starting from the oil market and then cascading onto stocks, bonds, and precious metals, will surely impact silver, and that impact is likely going to be on the downside because the global liquidity problems I have been perhaps the first to warn about are now worsening. This was confirmed by the latest statement of Indian Prime Minister Modi, who invited Indian citizens to stop buying physical gold for a year in order to ease the pressure on India’s central bank reserves and the Indian Rupee (”Modi Asks Indians to Stop Buying Gold, Hitting Jewelry Stocks”).

On the bright side, with demand for Solar Panels, Electric Vehicles, and high-performing battery storages, all items that require physical silver, increasing in a push to diversify away from crude oil dependence in the future, the long-term tailwinds behind silver remain strong.

Silver has delivered a powerful reminder of its upside when sentiment flips and price moves quickly. But the very factors that can drive outsized rallies also argue for patience when positioning after a sharp run. Right now, the market is not signaling an acute physical squeeze; at the same time, the macro backdrop remains fragile. The Strait of Hormuz risk has not been resolved; it has merely been underpriced by markets that have grown complacent. Any renewed disruption or escalation could force a new volatility regime across energy, equities, credit, and metals. In that scenario, silver’s sensitivity to liquidity and risk appetite matters: even if the long-term thesis stays intact, the short-term path can include sharp drawdowns as investors de-risk and dollar funding tightens. That is why, for now, the prudent stance is to avoid confusing a strong day with a durable new trend.