Two years ago, I wrote the article “NO, NVIDIA IS ONLY ONE PIECE OF A BIGGER (FRAUDULENT) PUZZLE”, trying to shine a light on what, two years later, became the biggest circular financing scheme in the history of financial markets. Since what I was describing at the time was hard to comprehend for most people, including those supposedly being “finance professionals”, the next day I wrote a simplified guide to explain the scheme: “HOW TO FABRICATE REVENUES FOR DUMMIES”

On Wednesday, Nvidia reported its earnings for the quarter ending in April 2026 and, two years later, there are plenty of signs warning that Nvidia is now dangerously close to hitting the brick wall of the great circular financing and revenues round-tripping scheme it was the very first to spearhead years ago, along with its two very first partners in crime, Microsoft and OpenAI (”THE SMOKING GUN THAT PROVES HOW OPENAI IS MICROSOFT’S REVENUES LAUNDROMAT”).

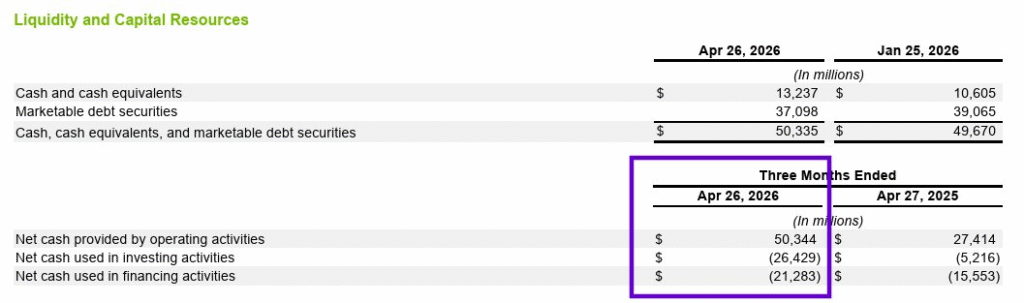

As you can see in the table below, while one year ago, Nvidia was re-investing about 57% of its operating cash flow back into its own customers and vendors, in the last quarter, this percentage rose to about 97%. Not surprisingly, Nvidia’s cash and equivalent accounts only rose by a meager ~$ 600 million in the last three months, despite its blockbuster revenue beat (as usual).

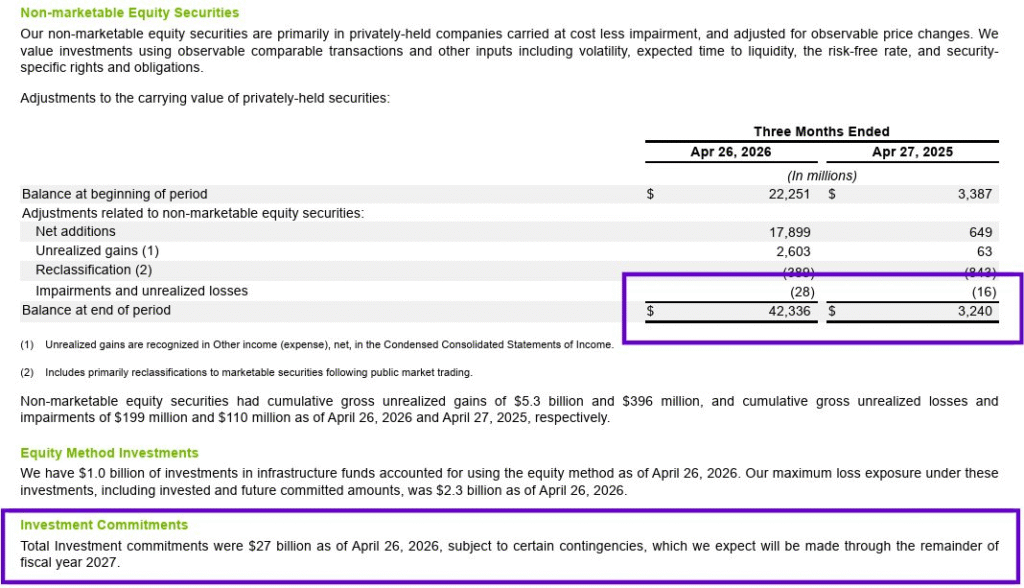

The extent to which Nvidia’s circular financing scheme had to gear up significantly over the past 12 months, in order to keep the wheel spinning and avoid an abrupt halt that would have nuked the whole AI narrative in the blink of an eye, can be observed in this second table.

Yes, my dear reader, Nvidia’s investments in “non-marketable equity securities” grew by a staggering 1,000%. That pile is also assured to continue growing in 2026 by another $ 27 billion, since that’s the amount Nvidia has already committed to invest. Intuitively, all signs point to a significant drop in cash and equivalents for Nvidia in the following quarter, and nobody should be surprised about that. In fact, if Nvidia wants to continue growing its revenues at the current pace, while the whole AI sector that is buying its GPUs still lags miles behind, the company will have to dig deep into its coffers. Personally, I would not even be shocked if, in several months, Nvidia surprises the market and tries to raise significant amounts of debt via bond issuances, like other hyperscalers such as Google, Amazon, or Oracle have already been forced to do in order to persist with their unrealistic Capex plans, praying the biblical amount of AI revenues they dream about finally materialise and they can finally start to recover the hundreds of billions of dollars they have spent so far.

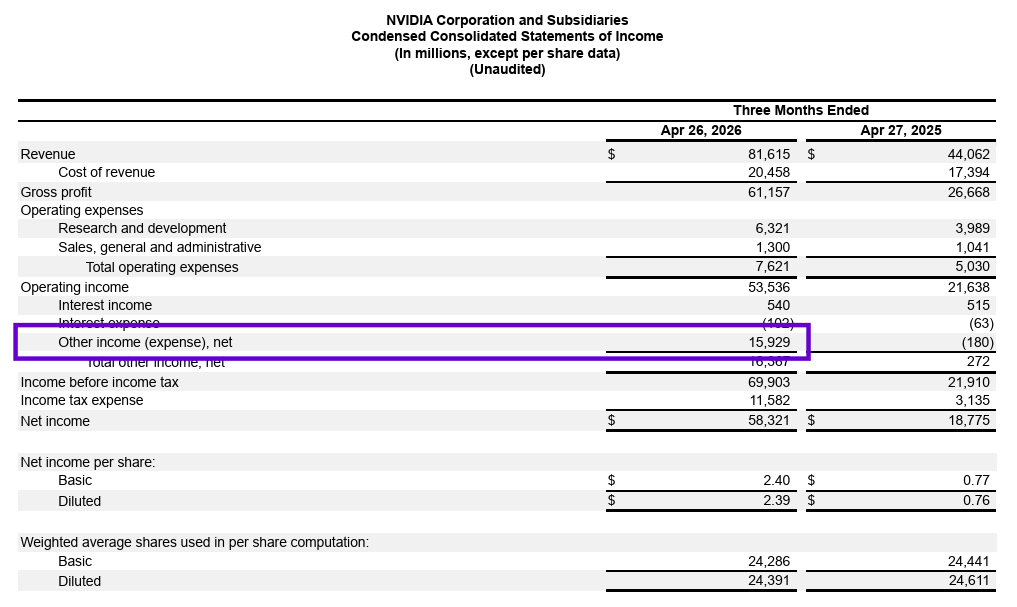

There are two other interesting details that Wall Street analysts and mainstream media have so far, maybe conveniently, missed in Nvidia’s latest earnings report. Both make you raise at least one eyebrow.

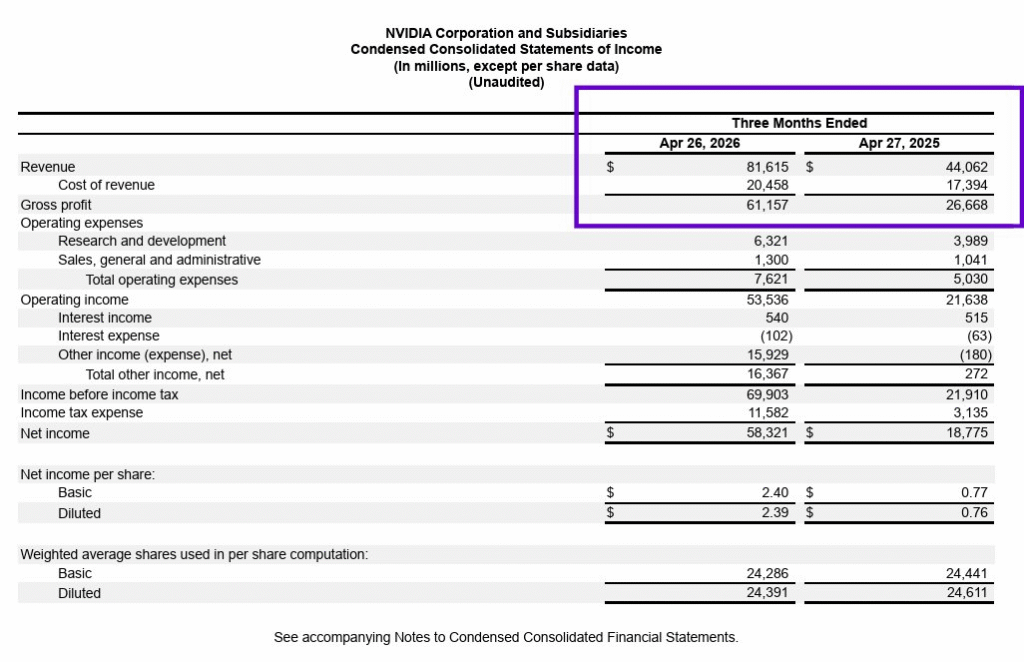

The first one is the incredible, not to say unrealistic, ability of Nvidia to deliver a massive upgrade of its GPUs (or so it claims), spending only 17% more to get those made by its own suppliers. The very same GPUs were then sold for a much higher price to customers, ultimately more than doubling the revenues earned compared to the same quarter in 2025. Let’s not forget that Nvidia DOES NOT RUN A SINGLE FACTORY, and all its production and supply chain is 100% externalized to third parties like TSMC that, oddly, reported a much higher growth in revenues than the increase in Nvidia’s cost of revenues. Yes, the math isn’t adding up, but who cares till the stock keeps going up, right?

The second remarkable item in the latest Nvidia earnings is the amount of unrealised gains the company booked, mostly from the increase in value of marketable security investments like CoreWeave or Intel, for a total of roughly $ 16 billion. Needless to say, without it, Nvidia’s bottom line and EPS would have missed analyst expectations brutally.

Nvidia’s latest quarter increasingly looks like a self-reinforcing loop: a growing share of operating cash flow appears to be recycled back into the same customer and vendor ecosystem that drives GPU demand, while overall profitability is meaningfully helped by unrealised gains on investments. If this “wheel” must keep spinning faster to sustain the current growth narrative, the next pressure points are cash balances and external financing, raising the odds of a sharp reassessment the moment counterparties, capital markets, or end-demand tighten. In short, the more the story depends on circular funding and mark-to-market boosts, the closer it gets to a brick wall.